Numerology, 2009 edition

Reader my friend, reader my Love,

Here comes the time of our now yearly installment, as du9 takes on the opportunity of the looming Angoulême Festival to try and paint the portrait of the little world of bande dessinée. (Of course, the English version somehow lacks this superb timing, but we still hope it will be of interest to our readers not versed in the intricacies of the French language) As usual, we are driven by curiosity and precision, with the aim of providing a clear and unabridged vision of the market in 2009. Welcome to a new installment of our “Numerology” — displaying the art of making numbers speak.

Last year, in the yearly bande dessinée special feature of industry publication Livres Hebdo, Fabrice Piault (assistant chief editor) was marvelling : “Every year, it comes as a new surprise. Indeed : overall, the bande dessinée market remains on a growing trend in 2008, for the fourteenth year in a row.”[1]

Fast-forward early 2010, and marvel has been replaced by relative moderation : benefiting from a “relatively serene economical context for 2009”, “for lack of being exceptional, the year has been acceptable”, with “a healthy market, but overall flat”.[2] Faced with such cautious reactions, it seems natural to try and go beyond the vague assertions to look more closely at the available data, so as to really know the extent of the damages.

And to know whether bande dessinée had also faced, in 2009, something of a crisis.

A market standing still

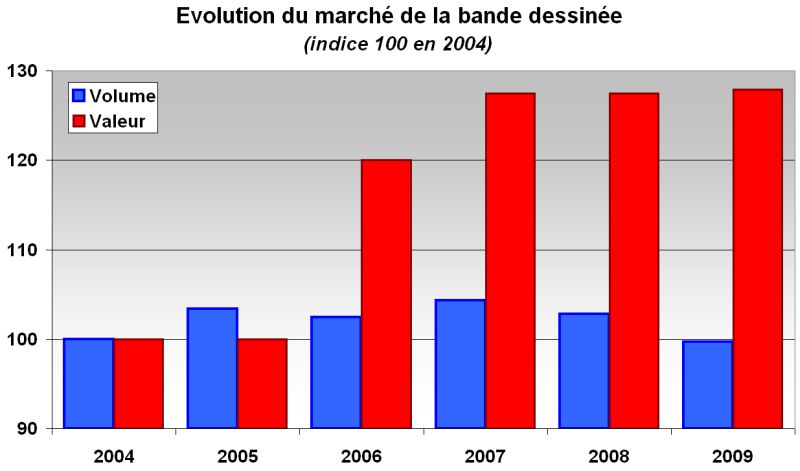

Diving in the figures, it quickly becomes apparent why Livres Hebdo is not as enthusiastic as in 2008 : according to IPSOS data, sales of bande dessinée at retail in 2009 are down 2.9 % in volume, and only register a tiny progression of 0.3 % in value. The French market would then amount to 33.6 million books sold, for 319.6 million euros. Would that mean that the upward streak lives on ? Fifteen consecutive years of growth, though modest, but of unabated growth ? Hold on.

Let’s look back : in January 2009, Livres Hebdo announced the market at around 328.8 million euros. But in the meantime, IPSOS has revised its estimate downwards and now sees a market in 2008 at 318.6 million euros — down a (microscopical) 0.03 % versus 2007.

Over the past three years then, the bande dessinée market is flat, slightly under the 320 million euros mark.

If the overall revenue remains stable, it is essentially because of the increase of retail prices (+3 % in 2009 at 9.80€) which compensates decreasing sales in volume — the past year’s downward turn being confirmed in 2009, and the market back to 2004 level.

| Average Prices | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 08=>09 |

|Albums| 8.3€ | 8.2€ | 10.3€ | 10.9€ | 11.2€ | 11.5€ | +3.3 %|

|Manga| 5.3€ | 5.3€ | 6.4€ | 6.6€ | 6,6€ | 6.8€ | +1.2 %|

|Overall| 7.6€ | 7.4€ | 9.0€ | 9.3€ | 9.5€ | 9.8€ | +3.1 %|

Struggling publishers

In the face of this (very) modest growth, Livres Hebdo wants to be reassuring, and states that “for the main publishers, sales have remained good” . Next page are given the market shares of those main publishing groups, which allows to make our own mind on the subject.

||Unit sales (in millions)||

| Publishing Groups | 2007 | 2008 | 2009 | 07=>08 | 08=>09 |

|Média Participations| 11.8 | 11,0 | 9.9 | -6.9 % | -9.5 % |

|Groupe Glénat| 5.4 | 5.4 | 4.9 | -0.2 % | -9.6 % |

|Groupe Flammarion| 3.2 | 2.6 | 2,7 | -19.3 % | 3.3 % |

|Soleil| 2.8 | 2.5 | 2.2 | -12.2 % | -10.8 % |

|Delcourt| 2.6 | 3.4 | 3.2 | 31.4 % | -3.9 % |

|Total Publishing Groups| 25.8 | 24.8 | 22.9 | -3.8 % | -7.6 % |

Quite surprisingly, 2009 is far from satisfying : excepted the Flammarion group (Casterman, KSTR, Jungle, AUDIE) which registers a slight progression of 3.3 % of its sales in volume, the four remaining leaders of franco-belgian bande dessinée see a serious decrease, with Soleil down by as much as 11 %.

For sure, this downward trend is nothing new : since 2002 (the first year Livres Hebdo communicated this kind of data), the marketshare controlled by the five largest publishing groups of bande dessinée has progressively decreased, from over 80 % in 2002 to barely 70 % in 2009. Over the course of seven years, the then-leaders Média Participations and Glénat have lost a lot of ground, Flammarion and Soleil have stood still, with Delcourt being the only publisher to register a strong progression of its marketshare (up from 4 % in 2002 to 9.9 % in 2009).

Faced with such an erosion, the main publishing groups all reacted in the same way : by increasing the number of releases, in the hope that this larger number of titles would counterbalance their failing sales. And indeed, over the course of 2009, there was talk of overproduction with much pointing towards the inflation on the number of titles accounted for in Gilles Ratier’s yearly inventory of the market. To wit, the number of yearly releases more than doubles over the 2003-2009 period, from 1730 titles to close to 3600.

Early 2009, in the yearly feature in Livres Hebdo, Philippe Ostermann (editorial director at Dargaud) seemed amazed : “I cannot even understand how one can release that many books.” And yet, Dargaud itself was not the last to follow suit, increasing from 88 titles in 2003 to 159 for 2009 (+80 %), the Média Participations group registering a 95 % progression.

| Evolution | 2003=>2006 |2006=>2009 |2003=>2009 | | Publishing Groups | Releases | Sales | Releases | Sales | Releases | Sales |

|Média Participations | +40 % | -4 % | +39 % | -9 % | +95 % | -12 % |

|Groupe Glénat | +17 % | -8 % | +35 % | -21 % | +58 % | -28 % |

|Groupe Flammarion | +37 % | -15 % | +3 % | +2 % | +42 % | -13 % |

|Soleil | +61 % | +51 % | +25 % | -25 % | +102 % | +14 % |

|Delcourt | +53 % | +122 % | +17 % | +12 % | +79 % | +149 % |

| Total Publishing Groups | +41 % | +5 % | +25 % | -10 % | +76 % | -6 % |

|Other Publishers | +85 % | +22 % | +13 % | +21 % | +108 % | +49 % |

|Overall Market | +63 % | +8 % | +18 % | -3 % | +93 % | +6 % |

The chart above also shows that this “race for production” is not a recent phenomenon. Yet, it also reveals that the increase in the number of releases over the past years that has been much criticized, is mainly due to the larger publishing groups (+25 % over the 2006-2009 period, versus +13 % for the rest of the market).

It has to be noted that the weight of those five large groups on the overall production has not changed much : while they represented 48 % of the yearly releases in 2003, they still amounted to 44 % of the releases in 2009 — this, despite the multiplication of publishing structures (up from 150 active publishers in 2001 to 288 in 2009), often mentioned as responsible for this unreasonable inflation.

At this point, it is important to remind our readers that the 4863 bande dessinée titles listed by Gilles Ratier for 2009 are far from being equals. Not only there exists wide discrepancies between the print runs of those books, but moreover, the distributors who usually work with the small press[3] do not have the same weight, and even less so the same coverage as the dedicated structures that the larger groups have established.[4] As a result, the “actual” burden of the new releases on the distribution channels (and therefore its supposed contribution to overproduction) is in no way comparable between the productions of the small press (with usually modest print runs) and those of the larger publishers.

Which means that should “traffic jams” occur in bookshelves, they are most likely due to the larger publishing groups, who have adapted to a context of higher rotation of titles[5] by increasing their presence in the distribution channel to maximize in-store presence. Some even resort to sending libraries books they did not order so as to force their hand.

The significant increase of the production then appears as a race forward, in the hopes of compensating the drop in sales. The larger publishing groups have no other choice than investing all the segments of the market considered as marginally interesting, be it manga or graphic novels.

To wit, the approach of the Futuropolis label (jointly owned by Soleil and the Gallimard group) sees the line with close to 200 books in its catalog after a mere four years of activity (4 in 2005, 36 in 2006, 39 in 2007, 55 in 2008, 55 in 2009), and has it reaching its “cruising speed”.

Moreover, it is to note that the revenues of the larger publishing groups do not rely solely on book sales, but also come from exploitation rights and licensed products. And indeed, Livres Hebdo dedicated three-quarters of its feature in 2009 to the “360-degrees approach”, especially regarding adaptations for the movie or the TV screen.

In 2010, most of the attention turned towards digital comics, in particular on mobile phones with Apple’s iPhone in the spotlight. Obviously, the iPhone is the only platform today to provide a simple, integrated payment solution, and it surely benefits from strong media coverage. But as Mourad Boudjellal (Soleil’s CEO) explained, this remains a “micromarket” with very low volumes and an extremely limited offer.[6]

Announcements of the creation new (digital) publishers are multiplying. The whole industry is holding its breath, waiting for the announcement of Apple’s iPad (which should be revealed at the end of January), bearing so many hopes. The digital revolution is most certainly on march — but the road is long, and for sure, the transition will be tough.

(Not so) sure wins

Beyond the overall evolutions of the market, which bring to light a fragile health, also appear some deep modifications in the sales repartition.

Indeed, over the past years we have seen a progressive decline of the importance of the top-selling titles. In 2001, the 50 titles listed in the yearly tops from Livres Hebdo/I+C controlled 28 % of the total market sales. Since 2006, this share has dropped to 13 %, indicating a growing dilution of purchases across a larger number of references. Yet, this weakening of the top 50 is not due to the sole expansion of the market — but also reveals a deep erosion of the performance of the best-selling series, especially obvious since 2006. Remarkably, 2007 was the first time since 2000 when no bande dessinée book sold over the symbolic mark of 300,000 copies in the year.

||Average yearly sales by tier||

| | 2000-05 | 2006-2008 | Evol. % | 2009 |

|Cumulated top 5 | 2.13m | 1.17m | -45 % | 1.26m |

|Cumulated #6-15 | 1.64m | 1.10m | -33 % | 1.04m |

|Cumulated #16-30 | 1.35m | 1.08m | -20 % | 0.93m |

|Cumulated #31-50 | 1.07m | 1.04m | -3 % | 0.94m |

|Cumulated top 50 | 6.19m | 4.40m | -29 % | 4.18m |

The cumulated sales of the yearly “top 5” have gone from an average of 2.1 million copies over 2000-2005[7] down to 1.2 million copies since 2006, or a 45 % decline. For reference, the cumulated sales of the titles between the 31st and the 50th rank remain stable at around one million copies, with only a minor, 3 % erosion.

The top-selling charts therefore show a significant compression, with a progressive reduction of the spread between the sales of rank #1 and rank #50.

||Evolution of the performance of new releases (end of year sales)||

| Series | Period | Sales | Print run |

|Astérix | 01 => 05 | -43 % | +6 % |

|Blake et Mortimer | 01 => 08 | -42 % | +20 % |

|Boule et Bill | 01 => 07 | -65 % | -30 % |

|Cédric | 02 => 08 | -55 % | -10 % |

|Lanfeust des étoiles | 01 => 08 | -34 % | -17 % |

|Largo Winch (Printemps) | 02 => 07 | -40 % | -18 % |

|Largo Winch (Novembre) | 05 => 08 | -9 % | -2 % |

|Le chat | 01 => 08 | -50 % | 0 % |

|Le petit Spirou | 01 => 07 | -67 % | -31 % |

|Les profs | 02 => 08 | -13 % | +100 % |

|Les Tuniques Bleues | 02 => 08 | -51 % | -19 % |

|Lucky Luke[8] | 04 => 08 | -67 % | -18 % |

|Spirou et Fantasio[9] | 04 => 08 | -48 % | -52 % |

|Thorgal | 01 => 08 | -43 % | 0 % |

|Titeuf | 02 => 08 | -44 % | +31 % |

|Trolls de Troy | 02 => 08 | -28 % | -11 % |

|XIII[10] | 00 => 07 | -40 % | +10 % |

Last year, we had witnessed the important erosion among established series, especially among the best-selling sales. In 2008, the 12th volume of Titeuf (Le sens de la vie) registered a performance down 44 % against the 9th volume (La loi du préau) published in 2002. Actually, the overall sales of the series saw a strong decline, down from 1.4 million copies in 2001 to 860.000 in 2008 — a 40 % drop.

This downward trend was also present for most of the classic Franco-Belgian series, with performances registering strong decline against the earlier years of the decade. Moreover, while sales were significantly down, initial print runs only presented minor adjustments, as the objective was to ensure a wide exposure at retail, even if it meant overprinting — a “missed” sale today being unlikely to be compensated later on. This way, the importance of the print run of a book now becomes a true commercial lever, and is no more the “reasonable” expression of an actual sales potential.

||Back-catalog sales (in thousand copies)||

| Series | Ave. 03-05 | 2009 | Evolution |

|Astérix | 814 | 532 | -35 % |

|Blake et Mortimer | 230 | 103 | -55 % |

|Boule et Bill | 358 | 244 | -32 % |

|Cédric | 372 | 125 | -66 % |

|Lanfeust des étoiles | 326 | 123 | -62 % |

|Largo Winch | 267 | 144 | -46 % |

|Lucky Luke | 312 | 181 | -42 % |

|Le petit Spirou | 150 | 55 | -63 % |

|Titeuf | 1 073 | 348 | -68 % |

|Les Tuniques Bleues | 265 | 176 | -34 % |

|Trolls de Troy | 190 | 112 | -41 % |

|XIII | 265 | 114 | -57 % |

Along with the decrease observed for the performance of new releases, sales of the back-catalog also present a significant downward trend.

Looking at the evolution of Lanfeust des Etoiles (-62 % in five years), the quote from Mourad Boudjellal (Soleil’s CEO) in Livres Hebdo that stated that the back-catalog was “back to its splendid form” somehow feels less convincing.

In fact, those well-established series have all been on the market for well over a decade, and their base of potential readers (already well exploited) is struggling to renew itself.

Note that those series were traditionally the cornerstones of the business models of the major publishers, who relied on regular releases and the solidity of those “brands” to secure their turnover. Indeed, over 2003-2004, the Glénat group realized no less than a quarter of its sales on the sole Titeuf series.

And most certainly the difficulties the major publishing groups are now facing find some of their roots in this “dependency” to recurring series, and the inherent “reader fatigue” that this model brings over time.

Manga at a standstill

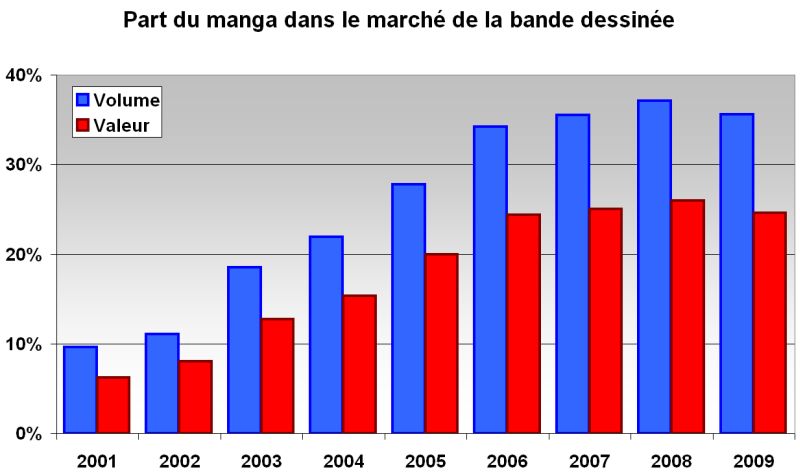

“Like the market of traditional bande dessinée, the manga segment saw its growth coming to a slowdown”, indicated Livres Hebdo in the introduction of its yearly feature. A slowdown, really ? More like a complete halt : indeed, for 2009 IPSOS gives manga sales down 6.9 % in volume and 5.8 % in value.

This is the first time that Japanese comics have stopped their growth (Livres Hebdo reluctantly recognizes “some exhaustion”), but its importance on the French market has stabilized for four years already, around 35 % in volume and 25 % in value. In fact, after the strong progression of the 2001-2006 period, sales have now plateaued, and the limits of the model are beginning to appear.

Indeed, the introduction of manga on the market managed to reach readers that have been so far overlook — teenagers (from 12 years up) on on hand, and female readers on the other, helped by a solid editorial system relying on a high frequency of publication in a context of constant solicitation. Moreover, manga has strongly participated in the process of self-identification of the young readers, which can be seen in the rise of a “manga culture”, as an element of differentiation and opposition against adults. Of course, the wide success of events like Japan Expo is another indicator.

The major publishing groups have been quick to identify that, and have heavily invested in the segment since 2005, searching for the next Dragon Ball. At end 2002, they only counted about thirty ongoing series. In 2003, they released another thirty new series on the market — the number of new series released every year going up to sixty for 2006-2008. At end 2009, the five largest groups had close to 150 ongoing manga series — to which one had to add the forty series or so that had reached their end (natural or anticipated) during the year.

||Number of new manga series per year[11] ||

| Group | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 |

|Média Participations | 1 | 5 | 8 | 7 | 13 | 14 | 17 |

|Groupe Glénat | 8 | 6 | 7 | 15 | 8 | 13 | 19 |

|Groupe Flammarion | 0 | 6 | 5 | 7 | 12 | 9 | 4 |

|Soleil | 8 | 2 | 10 | 16 | 16 | 14 | 19 |

|Delcourt (without Tonkam) | 9 | 9 | 9 | 14 | 10 | 11 | 11 |

|Total Major Groups | 29 | 34 | 39 | 59 | 59 | 61 | 70 |

Yet, the manga segment is highly concentrated, and depends essentially on a little number of best-selling series. There is a clear domination of recent productions geared towards teenagers (shônen / shôjo), to the detriment of classics or adult books. The three top-sellers control close to 30 % of the segment, and Naruto alone represents nearly one in seven manga books sold in France.

This situation is very clearly reflected in the initial print runs announced by the publishers. Naruto is at the top with 250,000 copies per volume, and keeps its followers at a safe distance : 85,000 copies for Soul Eater,[12] 80,000 for One Piece — considering all publishers, only eleven series enjoy print runs over 40,000 copies. For reference, there was in 2009 about a hundred books in Franco-Belgian series with initial print runs over this figure.

Moreover, the strength of manga relies in its high periodicity — the most active series having six, even seven new volumes released every year. Not only this publishing format quickly generates high sales volumes, but the subsequent recruiting of new readers comes fueling growth, as they try and catch up with the current publication. Yet, this strength ends up being its main weakness, and this for two reasons.

||Evolution of overal sales||

| Series | 07=>08 | 08=>09 | 07=>09 |

|Naruto | -7 % | -14 % | -20 % |

|One Piece | +19 % | +18 % | +40 % |

|Dragon Ball | -28 % | -18 % | -41 % |

|Bleach | +31 % | -14 % | +13 % |

|Fullmetal Alchemist | -19 % | -14 % | -30 % |

|Death Note | +55 % | -53 % | -27 % |

|Top 10 Series | -3 % | -13 % | -16 % |

|Manga segment | +3 % | -7 % | -4 % |

First, the publication pace remains dependent on the Japanese schedule, and catching up leads to a strong slowdown of releases (and therefore sales).

This is the case for Fullmetal Alchemist, which debuted on a pace of six yearly volumes, and had to drop to four volume in 2008 and only three in 2009 : over the course of two years, its sales have been reduced by 30 %.

Similarly, the series Kyo (38 volumes, ended 2008) and Fruist Basket (23 volumes, ended 2007) have disappeared from the top 10, after losing over 30 % of their sales in 2008. Dragon Ball keeps losing ground with a -18 % decrease of its sales, despite of yet another repackaging campaign with the Perfect Edition which debuted in 2009.

||Naruto Performance||

| Release | # | Sales | Evol. | Print Run |

|Jan. 2005| 15 |61,200| – |110,000|

|Jan. 2006| 21 |93,300| +52 % |130,000|

|Jan. 2007| 27 |130,900| +40 % |220,000|

|Feb. 2008| 34 |133,000| +2 % |220,000|

|Feb. 2009| 40 |138,000| +4 % |250,000|

Secondly, once the installation period is over (a period with strong growth), the long-running series move into cruise control with their sales more and more limited to the new releases. All potential readers have now been converted, and closely follow the publication schedule.

This phenomenon is apparent on Naruto : sales of the new volumes have plateaued since 2008 (after enjoying a two-digit growth until 2007), and 2009 sees a strong decrease of the sales of the back-catalog, down 22 % against the previous year.

Note that traditional Franco-Belgian series, which often rely on autonomous narratives (while most Japanese series rely on the serial formula) usually do not face this kind of problem.

After a difficult year in 2009, one would be hard-pressed to be optimistic for 2010. Indeed, Naruto, Bleach, One Piece and Negima ! should catch up with the Japanese publication, and therefore go from six volumes a year to four, in the best-case scenario. The slowdown observed for 2009 should be even more obvious for 2010, as the arrival of a new best-seller is unlikely with most of the high potential series already published. Interviewed by Livres Hebdo, Guy Delcourt indicated some anxiety, “even in Japan, where there aren’t many new big sellers”.

In this context, one can question the interest of releasing a series like Death Note (which counts only 13 volumes) at the high pace of a volume every other month. Surely, with cumulated sales of 1.3 million copies over three years, the operation did pay off. But this choice of “force-feeding” the readers by releasing series as fast as possible seems to be today the prevalent editorial approach, without trying to establish connections towards other manga series, or other bande dessinée titles in general.

The major unknown for 2010 though is the future strategy of the Japanese publishers, who have been very proactive by establishing a bridgehead on the market through the acquisition of Kaze last August by the Shôgakukan & Shûeisha Group. Taking into account the fact that the top four best-selling manga series in France are pblished by Shûeisha in Japan (Naruto, One Piece, Dragon Ball and Bleach), and that the two heavyweights come with the objective of “actively develop the market, by offering a larger variety of contents to our fans, in a shorter time and with increased efficiency”[13] … the situation of the French manga publishers for the coming year is far from serene.

2009 Top 50

A sure sign of a tight market, one can not that most of the big-sellers have been concentrated over the end of the year, in order to benefit the most of the “safety” of the Holiday season. Ignoring the Naruto titles, 9 out of the 10 top sellers have been released after September, with 8 of those published between October 14th and November 25th.

Released at end October (or the perfect timing for helping consumers struggling with their Christmas presents), the Asterix “golden book” brings some glitter to an otherwise lackluster year. Celebrating the sixtieth anniversary of the famous Gaul, this title did not benefit from the full aura of an actual new release, and it shows in its performance : released at the same time as Le ciel lui tombe sur la tête (in 2005), L’anniversaire d’Astérix et Obélix only manages 46 % of the sales of the former.

Ranking second, Blake & Mortimer keep on struggling. La malédiction des trente deniers sold 230,000 copies over six weeks, while the previous Les sarcophages du sixième continent (released in 2003 at a similar period) had sold 340,000 copies, indicating a 32 % decrease.

Completing the podium, Zep’s Happy sex ended up having far less impact as a new Titeuf album, despite an important media coverage turning its release into a mini-event. In fact, its performance is closer to that of Le Guide du Zizi Sexuel, an educative (and funny) spin-off title published in 2001.

Finally, the perfomance of the sixth volume of François Bourgeon’s Les Passagers du Vent is remarkable, fifteen years after the previous album in the series.

Speaking of series — in order to extend the concept, publishers try and turn their best-sellers into franchises : while XIII has reached its end in 2008, XIII Mystery carries on ; similarly, Lanfeust continues to see multiple sub-series, starting on an “odyssey” after having conquered the starts — all those parts linked in an overall continuity.

Yet, while the successive Lanfeusts register comparable performances, things are very different for what is perceived as derived products. To wit, the XIII Mystery titles manage at best a third of the sales of the main series at release. It will certainly be the same for Cixy de Troy, which benefited from a 90,000 copies print run but is not featured in the Top 50 Best-Sellers list.

Much has been said about the interesting potential of comics on the silver screen. Yet, the release of James Huth’s Lucky Luke featuring Jean Dujardin (and its 1.9 million tickets sold) did not have a significant impact on the sales of the series. The only title feature in the Top 50 is the most recent release, L’homme de Washington, released late in 2008 and which only registers residual sales at 56,000 copies sold over 2009.

To the contrary, the success of the comic book adaptation of The Simpsons is confirmed after last year’s solid start, and also benefits from some wide media coverage with the twentieth anniversary of the animated show. Publisher Jungle sees five of the eight released volumes among the Top 50, with global sales estimated around 300,000 copies for 2009.

To finish with, while it’s interesting to consider who’s featured among the 50 top-selling list, spotting who’s not there can reveal some surprises — titles with large print runs and high expectations, which ultimately fell short.

Among those, the volume 7 of the Murena series (Dargaud, print run of 150,000 copies), the Le Chat best-of (Casterman, 130,000 copies), the volume 6 of Le Donjon de Naheulbeuk (Clair de Lune, 120,000 copies), the volume 15 of L’élève Ducobu (Le Lombard, 120,000 copies), or the second volume of Tardi’s Putain de guerre ! (Casterman, 120,000 copies).

Conclusion

The past decade has seen the bande dessinée market register a modest progression, which now reveals its fragility. Over the last three years, sales in volume have decreased, while the overall turnover remains stable slightly under the 320m€ mark.

The major publishing groups, who dominated before, are now struggling to preserve their market share. The best-selling series which represented a large part of their turnover show signs of fatigue, for new releases as well as for the back-catalog.

In this context, the major publishing groups have strongly increased their production, in order to compensate for this revenue loss. The higher rotation of books in distribution channels has also encouraged them to maintain the initial print runs of high potential titles in order to maximize exposition at retail, even if it ends up increasing the number of returns.

Moreover, they have strongly taken position on the manga segment, whose growth has supported the market over those past years. This segment has experienced in 2009 its first year of decrease, and the conclusion or the slowdown of the best-selling series probably implies an even tougher 2010. Finally, the arrival of the Japanese publishers on the French market (through the acquisition of Kaze by the Shôgakukan & Shûeisha Group) might signify the end of this segment for the French publishing groups in the short term.

Finally, the topic of digical comics has frequently been in the spotlight throughout the year. Yet, this market is only in its early stages, and will take a few years to represent a significant outlet.

Let’s be straightforward : the bande dessinée market is facing a crisis. Yet, the limit of the model of recurring series only signifies the decline of a vision based on best-sellers. But the comic medium is not limited to creating “brands” — to the contrary, it has reached today an incredible depth and breadth, be it in its opening to the world, in the diversity of its topics, or in the energy of its creations. This is where lies its main strength, this is where lies its best chance.

Data and sources

The analyzes of this 2009 edition of our Numerology feature (or “the art of making numbers talk”) are based on two specific sources, except mentioned otherwise.

Regarding the accounting of the number of releases and the largest print runs, the yearly reports for the years 2001-2009 produced by Gilles Ratier, secretary of the ACBD (Association des Critiques et journalistes de Bande Dessinée).

Regarding actual sales figures, data from Livres-Hebdo/I+C over the 2001-2009 period. Additional data on manga have been graciously provided by IPSOS Média CT (Pôle Culture). We would like to express our thanks to Emmanuelle Godard for bearing with our requests.

1. Representativity of the IPSOS figures

Regarding the IPSOS panel, “the indicated figures are estimates based on actual sales (tracked at retail), from January 1st to December 31th, in metropolitan France, among a large and representative panel of retail locations.

This ranking takes into account all distribution channels with their respective market share : first and second level bookstores, large cultural outlets and general superstores. Excluded are export sales, sales in the French Overseas Departments and Territories, sales to wholesalers and online commerce.” (extract from the Methodological note attached to the top 50 best-selling bande dessinée chart in 2008)

Moreover, following an article in Le Figaro Magazine in July 2007 that questioned the quality of the Livres-Hebdo/I+C panel, Sophie Martin (General Director of the Ipsos Insight Culture department) indicated : “In five years, even if some end-year estimates have been the object of debate, the IPSOS ranking published by Livres-Hebdo and Le Nouvel Observateur has never been contested by publishers. It remains absolutely representative of retail book sales and is widely used by stores for their reorders and by publishers to adjust their print runs.”

The Livres-Hebdo/I+C data are widely recognized as representative of the market and used as such by the actors of the industry. The yearly rankings cover a constant perimeter (metropolitan France, excepted wholesales and online sales) — they therefore are comparable and cover the same “reality” of the market.

2. Consumer panels

While the Livres-Hebdo/I+C panel focuses on tracking the evolutions of the market in terms of sales, a certain number of studies try and analyze the population of comic book buyers and/or readers.

Indeed, the number of comic book buyers in France remains stable, representing around 10 % of the total population. (cf. “Le marché du livre en 2006” [The book market in 2006], study from TNS-Sofres, which confirmed a similar ratio over 2007.)

Regarding the comic book readership, the study “Les pratiques culturelles des Français à l’ère numérique” [Cultural activities of the French in the digital age] conducted by the Ministry of Culture and the INSEE (published October 2009) indicates that only 29 % of the French population aged 15 or more have read a comic book over the past twelve months (cf. this chart).

3. What about the other countries ?

A recurring attack against the IPSOS figures is that they only cover the French market, and do not account for the Belgian, Swiss and Canadian market. And that would inevitably invalidate the analyzes done on that truncated base. Yet, it is important to note that France represent more than 80 % of this francophone space, both in terms of population and in terms of book market — as well as bande dessinée.

Indeed, the French metropolitan population represents 62 million inhabitants, while the cumulated French-speaking populations of Belgium, Canada and Switzerland only represent 13.4 million souls.[14]

Moreover, an estimate of the French language book and bande dessinée market indicated for 2006 (in millions of euros) :[15]

||French language market (in millions of euros)||

|2006|France|Belgium|Switzerland|Canada|Total|France Share|

|Total books|4 100,0|253,4|77,9|328,0|4 768,9|86 %|

|Bande dessinée|300,0|38,7|11,9|16,4|367,0|82 %|

Of course, each territory presents its own specificities, and the trends observed with the Livres-Hebdo figures only cover the French market. Yet, this market has an overwhelming importance in the whole picture. For instance, to compensate a 5 % variation observed on the French market, the other three countries would have to present a variation of 23 % in the opposite direction.

Considering its weight (over 80 % of the French-language bande dessinée market), the evolutions of the French market therefore have an immediate (and important) impact on the industry in general.

4. The share of online sales

Internet penetration in households in France has seen a strong evolution over the past years, rising from 16 % in 2002 to 48 % in 2007. Following this progression, the general market has seen part of its revenue moving online over the past years, a part that is not covered by the Livres-Hebdo/I+C panel. This part is estimated today at around 10 % of the activity.

Yet, online sales follow very specific dynamics (known as the “long tail effect”), and see increasingly scattered sales in favor of references with very low levels of activity. If about 10 % of the total bande dessinée market is now sold through online sales, it is therefore probable that the importance of online sales for the best-selling titles is lower than this ratio.

It is important to keep in mind this market mutation, in particular when comparing different periods — a sales gap (downward) around 5 % between the years 2001-2002 and the years 2008-2009 is likely not significant.

Notes

- In the issue number 761, dated January 23, 2009, p.64-72.

- In the issue number 805, dated January 22, 2010, p.67-73.

- Le Comptoir des Indépendants, Makassar, La Diff, or even Harmonia Mundi. This list not aiming at being exhaustive, of course.

- DDL Diffusion, Delsol, Glénat Diffusion, Flammarion Diffusion, to only cover those belonging to the five largest bande dessinée publishing groups.

- Which one can observe in the contents of the yearly Top 50 published by Livres Hebdo. For the 2001-2004 period, about 20 out of the 50 best-selling references belonged to the back-catalog. Since 2007, this number is down to 11 titles released before the current year among the 50 best-selling titles, indicating a definite focus on newer releases.

- Across all operators, the French language offer on iPhone represented around 120 titles at end 2009. A drop in the ocean of close to 3,600 new releases every year…

- Voluntarily excluding the exceptional year 2001, with the 2.3 million copies of Astérix et la Traviata.

- The performance of the Lucky Luke book released in 2008 has to be put in perspective, as the title was only available for four weeks — compared to the three months of availability for the title released in 2004.

- Please note that the 50th volume of Spirou et Fantasio is not listed in the Top 50 sales for 2008 published by Livres Hebdo. We have considered the sales of the last ranked title to estimate the sales evolution.

- The conclusion of the XIII series in 2007 had seen two simultaneous releases. We have considered for this evolution the 18th volume, which had generated the largest sales.

- Monitoring conducted yearly by Mangaverse.

- At least for the first volume in the series, in order to ensure a good visibility at retail. The second volume, released simultaneously, had a more modest print run of 65,000 copies, with the following volumes for 2009 at an even more reasonable 61,000 copies.

- Excerpt from the official press release.

- Belgium : 10.4m inhabitants, with 40 % of French-speakers ; Canada : 33.2m inhabitants with 23.2 % of French-speakers ; Switzerland : 7.6m inhabitants with 20.4 % of French-speakers.

- Sources : France, SNE ; Belgium, Le marché du livre de langue française en Belgique (données 2006) ; Switzerland, Etude de l’Université de Zurich sur le marché du livre en Suisse ; Canada, Le marché du livre au Québec.