Numerology, 2010 edition

Reader my friend, reader my Love,

Here comes the time of our now yearly installment, as du9 takes on the opportunity of the looming Angoulême Festival to try and paint the portrait of the little world of bande dessinée. (Of course, the English version somehow lacks this superb timing, but we still hope it will be of interest to our readers not versed in the intricacies of the French language) As usual, we are driven by curiosity and precision, with the aim of providing a clear and unabridged vision of the market in 2010. Welcome to a new installment of our “Numerology” — displaying the art of making numbers speak.

[And if you so wich, you can download a nifty pdf file compiling this whole feature]

In a few words…

The bande dessinée market in France is facing a crisis and showing a significant decrease in 2010. The erosion of the “sure hits” of Franco-Belgian series (which concerns both new releases and back-catalog) is not compensated any more by the growth of the manga segment, which has reached a saturation point and is now on a downward trend.

In order to compensate for the decrease of sales on established series, publishers have starkly increased their production, by investing all segments of the market, and by trying to bring back value to their catalog through republishing programs. They have also maintained the initial print runs of high potential titles in order to maximize visibility at retail, even if this means increasing the number of returns. Publishers are still releasing an impressive number of new series on the manga segment, to counterbalance erosion dynamics and maintain their position.

Finally, the disappointing performance of the Top 50 best-selling titles in 2010 marks a decade worst, and only emphasizes the fragility of the industry today.

“The end of the bubble”

The title chosen by Fabrice Piault and Anne-Laure Walter for their annual feature on comic books in professional publication Livres-Hebdo[1] is quite telling. The time for rejoicing is over, and bande dessinée (until then celebrated for its remarkable performances) is now just one of the crowd. But right from the introduction, the tone is reassuring : “Let us not be doomsayers. The bande dessinée segment still evolves at a pace close to that of the overall book market, in spite of a slowing of sales and of bookstore frequentation in 2010. Yet, it is now proving mature for both its ‘Franco-Belgian’ side and the manga side, a more recent phenomenon.”

Sales are slowing indeed — IPSOS sees 2010 notably down, units sales losing 5.7 % and value sales registering a 2.0 % decrease. Actually, since 2006, the bande dessinée market is significantly down in units (-8.2 % according to IPSOS) and only progresses in value (+4.4 % in current euros) because of the sustained increase of average prices, which progressed an impressive +13.8 % over a five-year span.

||Average Prices||

| Year | Overall| Albums| Manga |

| 2006 | 8.96€ | 10.29€ | 6.39€ |

| 2007 | 9.35€ |10.87€ | 6.58€ |

| 2008 | 9.49€ | 11.16€ | 6.65€ |

| 2009 | 9.80€ | 11.48€ | 6.78€ |

| 2010 | 10.19€ | 11.96€ | 6.81€ |

| 06=>10 | +13.8 % | +16.2 % | +6.6 % |

Since 2005, the ‘album’ segment (for lack of a more appropriate name to encompass all that is not manga) has steadily declined, losing over 17 % of its sales in five years. This hemorrhaging has been temporarily compensated by the installation of manga on the market. Unfortunately, the manga segment reached its zenith in 2008, and is since on a downward trend with a severe -15 % over a two-year period.

For Livres-Hebdo, these are signs of ‘maturity’. Let us be blunt : bande dessinée is now officially facing a crisis.

Publishers showing a moderate optimism

Every year, Livres-Hebdo’s feature turns to publishers to get their feeling of the past twelve months. And every year, morale seems to be good — 2010 being no exception. Even if the introduction indicates that “last year, on the sales side, the segment mostly did damage control”, everyone is playing the same tune : Média-Participations claims a “healthy progression” while Dargaud “registers an exceptional year 2010” ; the Flammarion group rejoices about results “equivalent to those of 2009, which were very positive,” Delcourt achieved “nearly the same turnover as the previous year,” and finally for Glénat also, “the outcome has been positive.” There’s only Benoît Frappat, the new commercial director at Soleil, who is “more cautious,” and who acknowledges a “contrasted (year) across our catalogue, with a slight turnover decrease.”

Unfortunately, data published in Livres-Hebdo essentially cover unit sales of those five major publishing groups, which represent close to a cumulated 70 % of the market in 2010. Yet, one can still wonder about this “healthy progression” and those “positive outcomes” when the cumulated sales of those publishing groups are down 6 % in 2010… against 2009, which had already seen a 7.5 % decrease against the previous year.

||Unit sales (in millions)||

| Publishers | 2008 | 2009 | 2010 | 08=>09 | 09=>10 |

|Média Participations | 11.0 | 9.9 | 9.3 | -9.4 % | -6.0 % |

|Groupe Glénat | 5.4 | 4.9 | 4.6 | -9.6 % | -4.4 % |

|Groupe Flammarion | 2.6 | 2.7 | 2.4 | 3.4 % | -9.1 % |

|Soleil | 2.5 | 2.2 | 2.0 | -10.8 % | -8.5 % |

|Delcourt | 3.4 | 3.2 | 3.0 | -3.9 % | -5.7 % |

|Major Publishing Groups | 24.8 | 22.9 | 21.5 | -7.5 % | -6.2 % |

|Overall Market | 33.6 | 32.6 | 30.8 | -2.9 % | -5.7 % |

This is nothing new : the five major publishing groups are losing ground. Since 2002 (the first year when Livres-Hebdo started publishing this type of data), the market share they control has progressively decreased, from over 80 % in 2002 to just under 70 % in 2010. Over a 7-year span, the two leaders Média Participations and Glénat have lost a lot of ground, Flammarion and Soleil have managed to stay level, Delcourt being the only one to register a remarkable progression of its market share (from 4.0 % in 2002 to 9.9 % in 2010).

||Market Shares||

| Publishers | 2002 | 2010 | 02=>10 |

|Média Participations | 40.0 % | 30.4 % | -9.6 % |

|Groupe Glénat | 24.0 % | 15.1 % | -8.9 % |

|Groupe Flammarion | 9.0 % | 7.9 % | -1.1 % |

|Soleil | 6.0 % | 6.6 % | 0.6 % |

|Delcourt | 4.0 % | 9.9 % | 5.9 % |

|Major Publishing Groups | 83.0 % | 69.9 % | -13.1 % |

Let us be clear : it is not in our intent here to over-criticize those five major publishing groups. Yet, considering their importance on the market, the analysis of their positioning and of their strategic choices allow to explore the different dynamics at work, and shed some lights on the evolutions of the bande dessinée market over the past few years.

Classics on the decline

It is a fact : the “market blockbusters” are selling less than they used to. Between 2001 and 2010, cumulated sales of the yearly Top 50 published in Livres-Hebdo have been cut in half, from over 8 million copies at the beginning of the decade, to less than 4 million for the past year. Since 2007, a downward trend is present. Even the release of a new Titeuf in 2008 or the anniversary Astérix album the following year have not been able to correct the trend — even though those two franchises with alternating releases, had sustained a hefty share of the record performance over the years 2001 to 2002 with sales over 800,000 copies at each release. Such sales figures are now a thing of the past, and the old heroes are clearly tired.

It is important at this point to refute the idea of “blockbusterization” of the market that François Pernot evokes in the columns of Livres-Hebdo : “blockbusterization” would suppose increased sales for best-sellers, and a widening gap between the top of the charts and the other titles. In fact, to the contrary, this gap is closing over the years : in 2000, the #1 best-selling title was selling ten times more than the title ranked #50 in Livres-Hebdo’s yearly Tops ; in 2010, this ratio was down to five.

When considering the sales of the six most recent releases in the series regularly features in the yearly Livres-Hebdo Top 50, there is no denying this fact : most of these series are facing a significant and steady erosion (about 10 % with each new iteration) and are now seeing halved sales for their new releases.

Here are three additional observations :

– First, the rather ephemeral impact of Lucky Luke‘s “reboot” in 2004 (N-3 in the chart below), as three iterations later, the performance of Lucky Luke contre Pinkerton in 2010 represents only 46 % of that of La belle province ;

– Second, the difficulties faced by the XIII Mystery spin-offs (starting with N-2 in our chart), with a performance significantly under that of the original series — the most recent release only managing a quarter of the sales of the last XIII books in 2007 ;

– Finally, the marked decline of series targeted to kids, like Cédric (-42 % over the six last installments), but in particular Boule et Bill (-77 % over the past five) and Le Petit Spirou (-80 % over the past six).

| Releases[2] | Sales by Dec. 31st (000s)

|Initial print runs (000s)

|| Series | N-5 | N-4 | N-3 | N-2 | N-1 | ‘10 | Evol | N-5 | N-4 | N-3 | N-2 | N-1 | ‘10 |

|Largo Winch | 363 | 277 | 225 | 218 | 204 | 202 | -44 % | 556 | 530 | 500 | 455 | 490 | 470 |

|Lucky Luke | 161 | 161 | 412 | 232 | 137 | 189 | 18 % | 320 | 250 | 650 | 650 | 535 | 470 |

|Blake et Mortimer | 459 | 340 | 324 | 267 | 230 | 226 | -51 % | 500 | 600 | 520 | 600 | 500 | 450 |

|Le chat | 247 | 218 | 160 | 156 | 123 | 112 | -55 % | 320 | 300 | 375 | 320 | 320 | 300 |

|Lanfeust des étoiles | 156 | 138 | 107 | 127 | 96 | 72 | -54 % | 300 | 300 | 300 | 300 | 300 | 250 |

|Thorgal | 202 | 144 | 127 | 119 | 93 | 88 | -56 % | 350 | 280 | 280 | 250 | 300 | 250 |

|XIII | 316 | 247 | 286 | 99 | 81 | 73 | -77 % | 450 | 500 | 550 | 253 | 230 | 215 |

|Les profs | 97 | 95 | 80 | 66 | 58 | 53 | -45 % | 180 | 200 | 200 | 200 | 200 | 180 |

|Les Tuniques bleues | 89 | 74 | 63 | 62 | 50 | 57 | -36 % | 200 | 185 | 170 | 167 | 164 | 164 |

|Trolls de Troy | 119 | 102 | 94 | 92 | 76 | 68 | -43 % | 180 | 165 | 170 | 160 | 160 | 150 |

|Les schtroumpfs | 64 | 64 | ? | 46 | 46 | ? | ? | 150 | 140 | 125 | 150 | 140 | 140 |

|Le petit Spirou | 375 | 215 | 179 | 125 | 119 | 73 | -81 % | 600 | 590 | 600 | 415 | 330 | 290 |

|Boule et Bill | 345 | 181 | 144 | 120 | 79 | – | -77 % | 500 | 400 | 380 | 350 | 300 | – |

|Cédric | 103 | 85 | 71 | 64 | 55 | 60 | -42 % | 320 | 400 | 289 | 273 | 224 | 160 |

In spite of this marked decrease in sales, it is interesting to note that initial print runs only register moderate adjustments, as the objective remains to ensure a wide exposure at retail, even if it implies overprinting — missed sales today being unlikely to be made up for in the future. In Livres-Hebdo, Benoît Frappat (commercial director at Soleil) “observes in particular an increase of returns, as sell-in figures remain strong.” Meaning that a large print run for a book now becomes a commercial strength, and is no more the “reasonable” reflection of an actual sales potential.

Obviously, this downward trend for the largest sales impacts first and foremost the major publishing groups, and in particular the leading Média Participations. In fact, over the past ten years, the five largest publishing groups control in average 45 of the titles in the yearly Top 50, with Astérix (published by Editions Albert-René, now part of the Hachette Group) being the sole major exceptions. With an average 26 books in the top 50 over the last five years, Média Participations generates over 20 % of its yearly unit sales (or about 2.2 million copies).

Finally, it has to be noted that this erosion is not limited to new releases, but also extend to back catalog sales. Beyond the structural causes which could cause this evolution (increase of the number of new releases, limited shelf space in the face of a growing number of references, central ordering system, etc.), one can also wonder on the simple question of the age of those series, and that of their readership : in 2010, the top 10 best-selling Franco-Belgian books belonged to series aged (for the most part) 30 years or more.

In spite of the release of the second half of La malediction des trente deniers (with the two volumes featured in the Top 50 for 2010), the Blake et Mortimer series as a whole generated sales inferior to that of the single volume L’étrange rendez-vous at release a decade ago. Similarly, the release of the 17th volume of Largo Winch, Mer Noire, does not manage to push the performance of the whole series higher than the sales of the single Shadow (the 12th volume) in 2002. Overall, over the 2005-2010 period, the popular Franco-Belgian series register an erosion of their back-catalog sales of around 40 %.

Reacting to this phenomenon, Dupuis invested in a sustained program of revalorization of its catalog, through complete editions. As explained by Martin Zeller[3] (in charge of Dupuis’ complete edition program), this strategy presents numerous advantages :

– First, like for repackaging,[4] a complete edition creates a new reference,[5] which reintroduces in the distribution chain titles which probably had been excluded — and allow them to benefit from the exposure and visibility that new releases receive ;

– Second, the complete edition of a popular series presents a relatively low risk, even though (and that’s the downside) its potential success generally remains less important than for a true new release ;

– Finally, those complete editions also represent the opportunity for patrimonial projects, be it through the books themselves (series selection, critical apparatus) or in the preservation of the catalog through digitalization (a costly but necessary process).

Yet, it seems unlikely that those complete editions will recruit new readers in the short term : this strategy largely relies on nostalgia and the attachment of some readers to the “classics”.

A strong market seasonality

It’s been many years that books and bande dessinée feature in the top 3 Holiday gifts for the French : again for 2010, poll institute TNS-Sofres had them sharing the third place with apparel and lingerie, behind chocolates and money.[6]

The market seasonality clearly reflects this state of things : according to GfK, about a third of the bande dessinée sales (excluding manga) for the 2007-2009 period happened over the last two months of the year. Yet, it is interesting to note that the first quarter of the year (with the Angoulême Festival in January and the Salon du Livre in March, and the numerous accompanying releases) registers a performance significantly stronger than the slow period of April-October.

For a long time, publishers have adapted their release schedule accordingly, so as to benefit as much as possible from this dynamic. Most of the releases with large print runs (excluding manga) happen over the last part of the year — more precisely between early September and late November, when stores finalize their shelf content for the Holiday season. When considering titles with an initial print run of 75,000 copies or more, the period from August 20 to December 31 controls close to 60 % of the releases, and 70 % of the “shipping volume pressure” exerted by those titles on shelves.

Looking at the evolution of the situation since 2005, a slight increase in the number of those titles is present (from 32 in 2005 to 36 in 2010, or +12.5 %). Yet, it is difficult to decide on a possible strategy from publishers to position themselves on this key period : indeed, if the initial print run figures gathered by Gilles Ratier prove interesting, they are far from exhaustive, and their historical evolutions shows strong disparities (from 30 titles in 2010 to over 400 for 2010) and do not allow a global study without introducing an important bias. Therefore, we have chosen for consistency’s sake to limit ourselves to the production of the five major publishing groups, a perimeter on which the data gathered by Gilles Ratier seems to be the most satisfying in scope.

||Seasonality fof high potential titles (major groups)||

| | Full year |After August 20[7]

|Share | | Year | # | Cumulated

print runs | # | Cumulated

print runs | # | Cumulated

print runs |

| 2005 | 53 | 9.1 m | 28 | 5.8 m | 53 % | 63 % |

| 2006 | 43 | 7.6 m | 25 | 5.7 m | 58 % | 74 % |

| 2007 | 54 | 8.1 m | 22 | 4.4 m | 41 % | 55 % |

| 2008 | 44 | 8.9 m | 29 | 6.6 m | 66 % | 74 % |

| 2009 | 50 | 6.9 m | 31 | 4.5 m | 62 % | 66 % |

| 2010 | 52 | 8.5 m | 33 | 6.3 m | 63 % | 74 % |

| Average | 49 | 8.2 m | 28 | 5.5 m | 57 % | 68 % |

Two observations emerge. On one hand, there is a strong stability in the number of titles with an initial print run of 75,000 copies or more among the five major publishing groups (about 50 in average). On the other hand, it seems there is an increased focus on the key period of the Holiday season (from mid-August to mid December) over the past three years, with a record 33 titles for 2010, or 18 % over the average.

In fact, this apparent concentration is only linked to the coincidental alignment of the series’ release patterns — as it the surprising “stumble” of 2007. Indeed, considering the high print run series in the line-up of the five major publishing groups, it appears they are sufficient to account for the 2010 overcrowding : a rich year, as it benefits from a new release for most of those series, with the added contribution of the simultaneous release of a new installment for Joe Bar Team, Blacksad and Les Bidochon, three series which had only seen two releases each over 2001-2009.

| After August 20 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

| Total Number | 28 | 25 | 22 | 29 | 31 | 33 |

|Largo Winch | 1 | – | (March) | 1 | – | 1 |

|Lucky Luke | – | 1 | – | 1 | – | 1 |

|Blake & Mortimer| – | – | – | 1 | 1 | 1 |

|Le Chat | 1| – |1 | 1 | 1 | 1 |

|Le Petit Spirou | 1 | – | 1 | – | 1 | 1 |

|Thorgal| – | 1 | 1 | 1 | – | 2 |

|Lanfeust | 1 | 1 | 1 | 1 | 1 | 1 |

|XIII | 1| – | 2 | 1 | 1 | 1 |

|Titeuf(ou Zep) | 1 | 1 | – | 1 | 1 | – |

|Les Tuniques Bleues | 1 | 1 | 1 | 1 | 1 | 1 |

|Boule et Bill | (May) | – | (May) | – |1 | – |

|Occasional Hits[8] | 1 | – | – | 1 | – | 3 |

|Other series | 20 | 20 | 15 | 19 | 23 | 20 |

Regarding the high potential titles, the “Holiday season” appears to constitute of a rolling basis of about 20 titles, with the added contribution of the dozen of best-selling series which combined release patterns account for most of those past years’ fluctuations — 2010 being an example of a “perfect storm”.

This situation clearly concerns the publishers, who certainly fear cannibalization between those titles. Livres-Hebdo indeed indicates that the “ever-recurring issue of the industry of the concentration and the overcrowding of large print-run titles on second half of the year keeps on worrying the publishers, as no satisfying solution has been found to balance back the year in favor of the first half.”

Nevertheless, it is important to note that, as for its release schedule, the manga segment does not present a marked seasonality, and registers strong performances the year throughout. In particular, the last two months of the year only represent 20 % of the yearly sales (versus 33 % for Franco-Belgian albums). These two very distinctive consumption approaches might hint at a fundamental difference between the two segments : on one hand, manga books that are bought for oneself, relying on serial dynamics ; and on the other hand, Franco-Belgian bande dessinée with high-profile series often bought as gifts, relying part on habit, and part on the notoriety of those well-established brands.

Indeed, a close look at this release schedule reveals an almost “industrial” approach from the major publishing groups, displaying a certain habit for both release dates and initial print runs. To wit, the exemplar regularity of Philippe Geluck’s Le Chat, which always comes out mid-October with a 300,000 copies print run, more or less ; or that of Le Lombard with Léonard by Turk and de Groot, reliably out during the first half of March, with a print run around 80,000 copies ; or even the Blake et Mortimer books, a November feature (with the exception of Le Sanctuaire du Gondwana, released March 2008). For others, there are some slight adjustments, whether for Les Schtroumpfs (shifting to the first week of April, from their usual mid-January spot over 2005-2008) for a 140,000 copies print run, or the Lucky Luke (oscillating between early December and mid-October). Similarly, after establishing its success in mid-August (right before school starts back up), Bamboo has progressively shifted Les Profs to early October — with an initial print run now stabilized around 200,000 copies.

The forward race to overproduction

Faced with the strong erosion of their market share (and their sales), the main publishing groups all reacted in the same way : by increasing the number of releases, in the hope that this larger number of titles would counterbalance their failing sales. And indeed, over the course of 2009, there was talk of overproduction with much pointing towards the inflation on the number of titles accounted for in Gilles Ratier’s yearly inventory of the market. To wit, the number of yearly releases more than doubles over the 2003-2010 period, from 1730 titles to over 3800.

Early 2009, in the yearly feature in Livres-Hebdo, Philippe Ostermann (editorial director at Dargaud) seemed amazed : “I cannot even understand how one can release that many books.” And yet, Dargaud itself was not the last to follow suit, increasing from 88 titles in 2003 to 159 for 2009 (+80 %), the Média Participations group registering a 95 % progression. Early 2011, in Livres-Hebdo’s yearly feature, the same Philippe Ostermann keeps on regretting this endemic overproduction, “very perturbing for readers and buyers,” but does his best “by publishing only 110 to 115 books per year.” New releases, that is.

But the choice of focusing on the sole “new releases” significantly minimizes Dargaud’s contribution in particular,[9] and that of the Média-Participations group in general. Indeed, they have strongly invested in a republishing program, intent on revalorizing their catalog, either by the means of complete editions (Spirou & Fantasio, Jijé, Gil Jourdan, etc.) or through repackaging (“Black Edition” for Death Note or “Deluxe Edition” for Monster). While they represented 74 % of their overall releases in 2004, new releases only amount for 58 % of those for 2010 — a move that very is specific to the group, and which is nowhere to be seen among the other four leading groups. While the number of new releases shows an apparent stability for the group in 2010 (389 titles vs. 385 in 2009), the reality is in fact a 15 % progression for its overall production, new releases and republishing projects cumulated.

|Evolution | 2003=>2006 |2006=>2010 |2003=>2010 | | Publishing Groups | Releases | Sales | Releases | Sales | Releases | Sales |

|Média Participations | 40 % | -4 % | 57 % | -14 % | 119 % | -18 % |

|Groupe Glénat | 17 % | -8 % | 41 % | -25 % | 65 % | -31 % |

|Groupe Flammarion | 37 % | -15 % | -3 % | -7 % | 33 % | -21 % |

|Soleil | 23 % | 51 % | 23 % | -31 % | 51 % | 4 % |

|Delcourt | 53 % | 122 % | 26 % | 6 % | 93 % | 135 % |

|Major Publishing Groups | 34 % | 5 % | 31 % | -16 % | 76 % | -12 % |

|Other Publishers | 93 % | 22 % | 21 % | 16 % | 133 % | 42 % |

|Overall Market | 63 % | 8 % | 25 % | -8 % | 104 % | 0 % |

The chart above also shows that this “race for production” is not a recent phenomenon. Yet, it also reveals that the increase in the number of releases over the past years that has been much criticized, is mainly due to the larger publishing groups (+31 % over the 2006-2010 period, versus +21 % for the rest of the market).

It has to be noted that the weight of those five large groups on the overall production has not changed much : while they represented 50 % of the yearly releases in 2003, they still amounted to 43 % of the releases in 2010 — this, despite the multiplication of publishing structures (up from 150 active publishers in 2001 to 288 in 2010), often mentioned as responsible for this unreasonable inflation.

At this point, it is important to remind our readers that the 5165 bande dessinée titles listed by Gilles Ratier for 2010 are far from being equals. Not only there exists wide discrepancies between the print runs of those books, but moreover, the distributors who usually work with the small press[10] do not have the same weight, and even less so the same coverage as the dedicated structures that the larger groups have established.[11] As a result, the “actual” burden of the new releases on the distribution channels (and therefore its supposed contribution to overproduction) is in no way comparable between the productions of the small press (with usually modest print runs) and those of the larger publishers.

In order to illustrate this state of things, let us consider a (very) simplified example of the situation. If 50 small press publishers each publish three books, with a 1,000 copies print run (which is not unrealistic), they represent a “cumulated load” of 150,000 copies on the distribution chain. If we now consider Flammarion (ranked seventh among publishing groups according to the number of releases listed by Gilles Ratier), their 150 new releases with an average 10,000 copies print run (for ball-park figures) represent for the year a “load” of 1.5 million copies. It quickly becomes obvious how, with a similar release production (150 new titles in each case), the “load” on the distribution/retail chain i.e. the “overproduction,” is of a completely different scale between small press publishers and large publishing groups. In this over-simplified example, small press publishers represent an impressive 50 % of all releases, but a mere 9 % of the copies present on the shelves.

This means that should “traffic jams” occur in bookshelves, they are most likely due to the larger publishing groups, which have adapted to a context of higher rotation of titles[12] by increasing their presence in the distribution channel to maximize in-store presence. Some even resort to sending libraries books they did not order so as to force their hand.

Graphic novels

As we’ve just seen, the significant increase of production is a forward race in order to try and compensate for the erosion of sales. The major publishing groups have no choice but to invest all segments that present some potential, be it manga or the graphic novel.

In order to explore this latter point in particular, it is necessary to turn again to the yearly reports from the ACBD — and in particular the annexes, which list in detail yearly releases by publisher.

If those pages prove particularly rich in information, it is important to avoid delving too much on the charts and the evolution graphs by segment : indeed, the chosen classification is far from perfect and is likely to lead to erroneous conclusion.

Thus, Gilles Ratier considers four segments to study the evolution of the number of new releases throughout the years : manga, alternative press, major publishers and comics. On one hand, this segmentation mixes book provenances (manga and comics) and publisher sizes (large or alternative) — even though the major publishing groups do publish a large number of manga and comics, which are therefore not counted in the evolution of their production.

On the other hand, the denomination of “alternative press” is misleading and covers a reality far from the usual acceptation of the term : indeed, while the “major publishing groups” are limited to the five leading groups (Média-Participations, Glénat, Delcourt, Flammarion and Soleil), the “alternative press” includes… all that remains. One will find under this moniker a certain number of large publishing groups (among which Hachette, Panini, Gallimard, Bayard-Milan, Editis), as well as publishers like Kazé, Bamboo, Joker or Ankama, whose editorial approaches are extremely different from those usually associated with the “alternative” label.

It is therefore necessary to reconsider those evolutions by going back to the individual publisher listings, to recreate a more truthful image of the market’s reality. This recomposed picture highlights the increased competition on the segment of the alternative press (in its traditional acceptation of “auteur comics”), both through the introduction of new publishing structures, and first and foremost by the positioning of the major publishing groups.

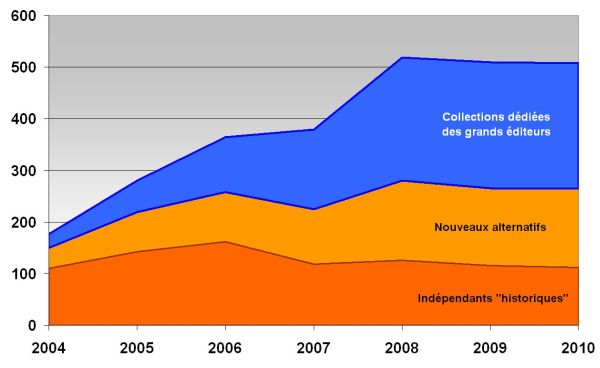

Over a seven-year span, the “graphic novel” segment has faced a profound mutation, and is now particularly crowded. Since 2004, the number of yearly releases has increased threefold, jumping from 150 books to over 500 books in 2010. Over this period, the “historical indies”[13] have maintained a level production or around 110 yearly releases. Similar structures, which we will call the “new alternatives”[14] (for lack of a better name) have appeared and/or developed their offer to represent in 2010 a comparable production in terms of number of releases.

But most important is the massive arrival of the major publishing groups, through their specific labels[15] (and for a few, helmed by names that emerged from the “historical indies”, as is the case for the Shampooing collection at Delcourt under Lewis Trondheim’s responsibility, or the Bayou collection at Gallimard Jeunesse headed by Joann Sfar), which represent today half of the segment’s overall production.

Here we see at work the “overtaking” dynamic evoked by Jean-Christophe Menu in Plates-bandes, his essay/pamphlet of 2005, and further developed by Morvandiau in his text published in the Monde Diplomatique in January 2009,[16]) “Les indépendants défendent leurs cases” :

“It never takes long to the bande dessinée industry to pick up formats that have been initiated by others, as well as recruiting part of the authors who appeared through this movement, leading it to (re)gain some legitimacy by appearing in medias perceived as opinion leaders. In spite of the worldwide success of one Persépolis, the recycling strategy of the commercially-minded publishers (and the groups that control them) therefore tends to dissimulate the singularity of those who advocate, first and foremost, an artistic-driven approach.”

Manga on the decline

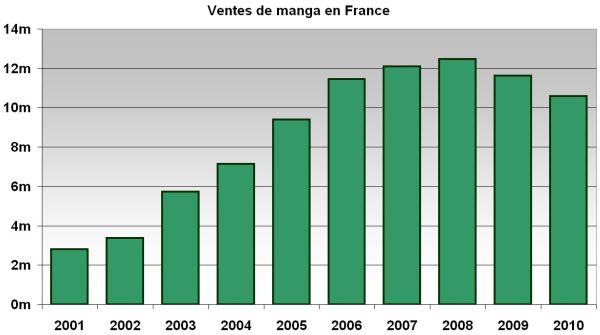

The golden days of manga are clearly behind us. The segment, which proved particularly strong over the past decade, peaked in 2008 (with close to 12.5 million copies sold) and subsequently decreased afterwards, now representing around 11 million copies sold yearly. The contribution of manga to the overall market in 2010 is back to its 2006 level, with slightly more than a third of the total unit sales, and slightly less than a quarter of the total value sales.

||Manga share in the bande dessinée market||

| | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

|Unit sales | 9.6 % | 11.1 % | 18.5 % | 21.9 % | 27.8 % | 34.2 % | 35.6 % | 37.2 % | 35.6 % | 34.4 % |

|Value sales | 6.2 % | 8.0 % | 12.7 % | 15.3 % | 20.0 % | 24.4 % | 25.3 % | 26.1 % | 24.6 % | 23.0 % |

The saturation of the segment is now obvious, after a few years of remarkable growth. Indeed, the introduction of manga on the market managed to reach readers that have been so far overlook — teenagers (from 12 years up) on one hand, and female readers on the other, helped by a solid editorial system relying on a high frequency of publication in a context of constant solicitation. Moreover, manga has strongly participated in the process of self-identification of the young readers, which can be seen in the rise of a “manga culture”, as an element of differentiation and opposition against adults. Of course, the wide success of events like Japan Expo is another indicator.

Yet, the manga segment is highly concentrated, and depends essentially on a little number of best-selling series. There is a clear domination of recent productions geared towards teenagers (shônen / shôjo), to the detriment of classics or adult books — a point duly noted by Livres-Hebdo this year : “publishers are trying to recruit new readers, especially on the manga segment, which suffers from a lack of readership renewal.” The three top-sellers control more than a quarter of the segment, and Naruto alone represents nearly one in seven manga books sold in France.

This situation is very clearly reflected in the initial print runs announced by the publishers. Naruto is at the top with 250,000 copies per volume, and keeps its followers at a safe distance : 80,000 copies for Fairy Tail, 90,000 for One Piece — considering all publishers, in 2010 only nine series (versus 11 in 2009) enjoy print runs over 40,000 copies. For reference, there was in 2010 around a hundred books in Franco-Belgian series with initial print runs over this figure.

Betting on new releases

As early as 2005, the major publishing groups have heavily invested in the segment since 2005, searching for the next Dragon Ball. At end 2002, they only counted about thirty ongoing series. In 2003, they released another thirty new series on the market — the number of new series released every year going up to sixty for 2006-2008, even though the market was giving the first signs of slowdown.

Yet, as is shown on the chart below, the number of new series launched on the francophone market has not decreased over the past years — quite the contrary, as 2009-2010 remain on cruise course with 70 new series for just the five main publishing groups. One should wonder about the rationale behind this strategy in a context of a saturated market, facing a strong decline.

| Number of new manga series launched each year[17] |On-going |

| Publishing Group | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | Series |

|Média Participations | 1 | 5 | 8 | 7 | 13 | 14 | 17 | 19 | 49 |

|Groupe Glénat | 8 | 6 | 7 | 15 | 8 | 13 | 19 | 14 | 40 |

|Groupe Flammarion | 0 | 6 | 5 | 7 | 12 | 9 | 4 | 2 | 7 |

|Soleil | 8 | 2 | 10 | 16 | 16 | 14 | 19 | 25 | 39 |

|Delcourt (Tonkam excluded) | 9 | 9 | 9 | 14 | 10 | 11 | 11 | 11 | 26 |

|Major Publishing Groups | 26 | 28 | 39 | 59 | 59 | 61 | 70 | 71 | 161 |

First, it is important to note that among the best sales by franchise on the French market for 2010, two manga (Naruto and One Piece) are at the two top spots, with four others (Fairy Tail, Dragon Ball, Bleach and Fullmetal Alchemist) in the Top 15. Their performance is even more impressive when compared to that of Astérix, the first Franco-Belgian property : twice the sales in 2010 for One Piece, and nearly three times as much for Naruto, all issues cumulated. It is no mystery then that manga remains very attractive for publishers who concede that “the market is showing a strong resistance to new series” (Guy Delcourt, in Livres-Hebdo).

Moreover, the strength of manga relies in its high periodicity — the most active series having six, even seven new volumes released every year. Not only this publishing format quickly generates high sales volumes, but the subsequent recruiting of new readers sustains growth, as they try and catch up with the current publication. Once the installation period is over (a period with strong growth), long-running series move into cruise control with their sales more and more limited to the new releases. All potential readers have now been converted, and closely follow the publication schedule.

This phenomenon is currently apparent on Naruto : sales of the new volumes have plateaued since 2008 (after enjoying double-digit growth until 2007), and 2010 sees a strong decrease of the sales of the back-catalog, down 22 % against the previous year. By the way, it is highly probably that One Piece, the #2 series on the segment, will face a similar evolution in 2011 : after two years of strong growth, sales of One Piece have seen a limited progression in 2010 (+4 %), probably reaching the peak of the installation period.

||Naruto Performance||

| Release | # | Sales | Evol. | Print run |

| Jan. 2005 | 15 | 61 200 | – | 110 000 |

| Jan. 2006 | 21 | 93 300 | +52 % | 130 000 |

| Jan. 2007 | 27 | 130 900 | +40 % | 220 000 |

| Feb. 2008 | 34 | 133 000 | +2 % | 220 000 |

| Feb. 2009 | 40 | 138 000 | +4 % | 250 000 |

| Jan. 2010 | 46 | 120 700 | -13 % | 250 000 |

||Overall sales evolution||

| Series | 07=>08 | 08=>09 | 09=>10 |

|Naruto | -7 % | -14 % | -14 % |

|One Piece | +19 % | +18 % | +4 % |

|Fairy Tail | – | – | +29 % |

|Dragon Ball | -28 % | -18 % | -34 % |

|Bleach | +31 % | -14 % | -15 % |

|Fullmetal Alchemist | -19 % | -14 % | -20 % |

|Top 10 Series | -3 % | -13 % | -12 % |

|Manga segment | +3 % | -7 % | -9 % |

The law of series

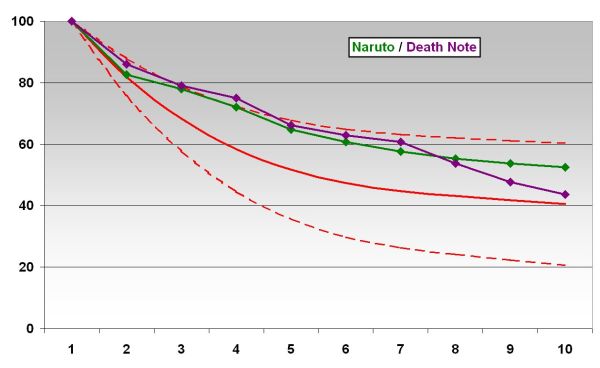

These dynamics at work during the installation of a series are complemented with another one, linked to the serial nature of most of manga series. The key advantage of a strong readership loyalty is also its major weakness, as each new installment sees an erosion of this readership, a phenomenon that can take serious proportions over time.

In our analysis of data on manga in the US market conducted in June 2010[18] highlighted very similar erosion dynamics for all titles. We had identified a median hypothesis (which saw the tenth volume in a series generate 40 % of the life-to-date first volume sales), as well as a high hypothesis (at 60 % of the first volume sales) and a low hypothesis (at 20 %), covering the whole range of performances, from commercial failure to average sales to full-out success. Unfortunately, the partial data available for the French market do not allow us to conduct the same analysis, but they seem to indicate that similar dynamics are at work here.

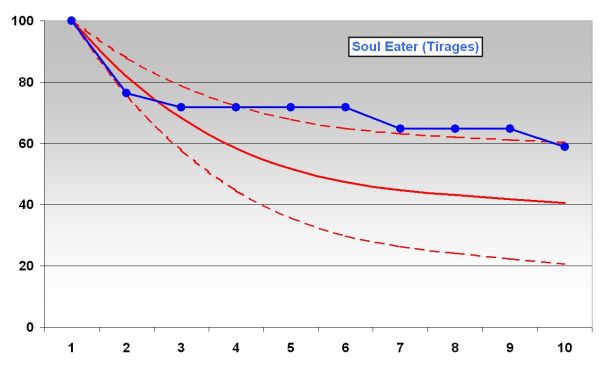

If most publishers are on autopilot, with all releases for the year within a given series benefit from the same print runs (an attitude not unlike the industrial approach we outlined earlier with the Franco-Belgian series), a few of them obviously take into account this element of the market. It is often the case for the first volumes in a series. To wit in 2010, the first two volumes of Dragon Ball Z : cycle 3 by Glénat Mangas had print runs of 38,000 copics, versus only 30,000 for the following two volumes. Yet, this approach is rarely extended to cover the whole run of a series, which makes Kurokawa’s strategy on Soul Eater even more remarkable, with the successive print runs of the first twelve volumes closely following erosion dynamics.

Finally, it is important to remember that the publication pace remains highly dependent on the Japanese serialization, which causes a significant slowdown of releases (and therefore sales) once the catch-up phase is over. This has been the case for Fullmetal Alchemist, which started off on a six-books-a-year pace, but was down to four in 2008, three in 2009 and eventually only two in 2010. Over a three-year span, its sales have seen a 45 % decrease.

Similarly, series like Kyo (38 volumes, ended 2008) and Fruits Basket (23 volumes, ended 2007) disappeared from the Top 10 after losing over 30 % of their sales in 2008. As for Dragon Ball, the series is still losing ground and has registered a 60 % sales decrease in three years despite yet another “repackaging” campaign with the Perfect Edition, which publication debuted 2009 and is still on-going.

Moreover, during the course of 2011, Naruto, One Piece and Bleach should catch up with the Japanese publication, and eventually drop from six books a year to four, in the best case — with serious consequences on the overall health of the segment for 2012. In this context, one can question the interest of releasing a series like Death Note (which counts only 13 volumes) at the high pace of a volume every other month. Surely, with cumulated sales of 1.3 million copies over three years, the operation did pay off. But this choice of “force-feeding” the readers by releasing series as fast as possible seems to be today the prevalent editorial approach, without trying to establish connections towards other manga series, or other bande dessinée titles in general.

As the major publishing groups have become highly dependent on manga for their revenues, launching new series becomes a necessity. On one hand, erosion dynamics do not allow to rely solely on exploiting already established series (which are also exposed to the risk of slowdown in case of catch-up with the Japanese publication), requiring to look for new blood. On the other hand, the same erosion dynamics favor “#1 volumes” over the following ones. This situation is not much different from what happened on the US market in the early 90s, when collector speculation had led to a multiplication of “#1 issues” (and alternate covers) from Marvel in particular.

The patrimonial approach

While the success of manga essentially realied on the shônen and shôjo production, and first and foremost established itself as a generational read, the publishing of patrimonial works from Japan remains largely marginal. Dedicated labels are rare (“Vintage” at Glénat, “Classic” at Taifu or “Sensei” at Kana, with the addition of the the “Tezuka” collection at Asuka) and limited to a handful of names. In fact, it appears that the “discovery” of some patrimonial authors often relies on a publisher’s capitalizing on a “brand” combining critical acclaim and commercial performance, as is the case for Taniguchi Jirô (shared between the écriture and Sakka collections at Casterman) or Hirata Hirochi (at Delcourt).

At Kana, the “Sensei” collection (“the collection of the masters of manga”) is rather emblematic in the way it approches the patrimonial issue. First, its whole catalog sees the “masters of manga” limited to a meager sample : 23 published volumes for no more than five authors,[19] with an overwhelming domination of the now well-known figure of Kamimura Kazuo. Indeed, he represents 11 of the 23 volumes released since the collection was launched at end 2007 — and 8 of the last 13 books released over the September 2009-January 2011 period. Second, this collection is mostly made of “short” formats, mainly trilogies and tetralogies, with a couple of one-shots thrown in.[20] Considering the small volumes that this type of publication usually generates, this strategy allows avoiding strong erosions over time, and could even encourage consumers to complete a series they have started : buying the last volume of a trilogy should be a lesser commitment than investing in the third volume of a series with at least a dozen to follow. Using the standard erosion model, it appears it is more interesting (from a financial point of view) to release four thick 1500-page volumes for 29€, than twelve 500-page volumes at 12.50€.

The 2010 Top 50

Laden with expected best-sellers, there is no doubt that 2010 ended up disappointing with cumulated sales for its Top 50 under the 4 million copies mark[21] — the first time it happened to our knowledge, the available data going back to 2000. The blame goes to an anemic Top 5, which (again, for the first time) does not break the million mark, seriously casting doubt over Livres-Hebdo’s claim that “if the bande dessinée market resists, it is first and foremost thanks to the titles with large print runs scheduled for the end of the year.”

Indeed, many hopes were riding on the supposed strength of this exceptional quartet (Joe Bar Team, Blake et Mortimer, Largo Winch and Lucky Luke), which had not been present together for a long time. One can even wonder if the saying shouldn’t be rephrased in “more is less”, with all those books with stellar print runs eventually ending up competing too much with themselves… Surprisingly though, we had faced a similar situation back in 2004, with the same four series and the addition of a new XIII and (more importantly) a new Titeuf, then at its peak.

The verdict : 1.35 million copies in 2004, versus barely over 840,000 in 2010, or an overall performance down by 38 % for those four new releases. More than cannibalization, this is the work of the series erosion (which we covered earlier).

While the manga segment is significantly hitting a slowdown, Japanese series have never been as present in the Top 50, with no less than 14 titles across three series (Naruto, 7 books ; One Piece, 4 books, and Fairy Tail, 3 books). This situation summarizes well the nature of the segment, very concentrated and relying on serial dynamics.

Another notable element is the performance of two series targeted at a younger audience (9-12 year old) on which manga are relatively less present. Julien Neel’s Lou ! has three books in this Top 50 (despite having no new release), as well as Patrick Sobral’s Les Legendaires, whose style is clearly influenced by the Japanese productions.

Strong on their TV-based notoriety, The Simpson are now well established in the top sales of the bande dessinée market in France. They have three books in the Top 50, and solidify their #3 ranking among the best-selling series for 2010 (and the top one when excluding manga) with over half a million copies sold.

While the major publishing groups are intent on developing their media-mix in order to adapt their brands on multimedia supports (be it TV shows, videogames or others), the success of the comic books derived from the show created by Mat Groening underlines the specificity of this model. Indeed, an adaptation on another media feeds on the popularity of the initial work, the reverse being far less likely — to wit, the negligible impact on the sales of Largo Winch or Astérix aux Jeux Olympiques of the launch of the corresponding movies.[22]

On the graphic novel side, La position du Tireur Couché (adapted from Jean-Patrick Manchette’s novel) consolidates Tardi’s exceptional position as one of the rare artists acknowledged as such by the generalist cultural press, and still managing to appear in the best-seller Top 50 without bowing down to the series format. Similarly, the critical success that welcomed Christophe Blain and Abel Lanzac’s Quai d’Orsay makes it the sole surprise of this Top 50 with over 70,000 copies sold. Besides its narrative qualities, the political subject of this book (and its original approach) has certainly boosted its sales, as it had been the case for La face karchée de Sarkozy by Cohen, Malka and Riss over 2006-2007. Yet, other attempts on a similar theme have proven far less successful, be it Les aventures de Sarkozix at Delcourt, or Sarkozy et ses femmes in the Drugstor collection at Glénat.

To finish with, it is interesting to highlight the titles not present in this list, and which, in spite of strong initial print runs (and corresponding sales objectives) have failed to break the #50 level, with its 42,900 copies sold by December 31st.

Among them : the 5th volume in the Game over series (Dupuis, 150,000 copies print run), the 8th volume of Les Blagues de Toto (Delcourt, 150,000 copies), the 25th volume of Yoko Tsuno (Dupuis, 150,000 copies), or the 28th volume of The Smurfs (Le Lombard, 140,000 copies).

Likewise, the prequel Troisième Testament : Julius (Glénat, 150,000 copies) is not featured in this Top 50 ; neither is the 51st volume of Spirou et Fantasio in spite of the arrival of a new creative team (Yoann and Fabien Vehlmann, at Dupuis, 110,000 copies) or the 5th volume of Magasin Général (Casterman, 100,000 copies).

To finish with, some “concept series” show a strong decline, as is obvious with the last two releases in the Blondes series (volumes 12 and 13) which, in spite of a print run stabilized at 100,000 copies, do not manage to break into the Top 50 after the “high” times of 2005-2007.

Conclusion

As the market figures are for the first time significantly in the red, it is important to note how deeply-rooted the current crisis of the bande dessinée market is. The limits of both the Franco-Belgian series model (based on yearly releases), and the intensive exploitation of manga (which largely supported the market growth over the past years) are now clearly apparent.

In order to compensate the erosion of yesteryear’s sure hits, the major publishing groups have significantly increased their production. Combined with the multiplication of publishing structures in general, this has resulted in overproduction, which consequently weakens the chain upstream of book retailers (authors, publishers, distributors), who are more and more reduced to a role of warehouse management.

The digital revolution, already announced two years ago,[23] is still not underway, and only represent at best, marginal revenues, at worst, a laboratory for experimentation for the future. Even more, the agitated discussions around the question of royalties have put to the fore the tensions and unease that reign in the relations between publishers and authors, in the face of a future that has never been so uncertain.

In particular, the progressive pauperization of authors jeopardizes in the mid- to long-run the existence of full-fledged carrier artists, closing in on the situation of the book industry in general.

And yet, the bristling offer available today reminds us how much bande dessinée is, even before becoming a “brand” or a product, a question of stories and character, of singular voices and audacious visions, of outlooks on the world and shared emotions. The bande dessinée industry might be facing a crisis — but bande dessinée itself still holds many treasures for those who know how to find them.

Data and sources

The studies and conclusions of this 2010 edition of our Numerology feature (or “the art of making numbers speak”) are based on two specific sources, except mentioned otherwise.

– Regarding the accounting of the number of releases and the largest print runs, the yearly reports for the years 2001-2010 produced by Gilles Ratier, secretary of the ACBD (Association des Critiques et journalistes de Bande Dessinée) ;

– Regarding actual sales figures, data from Livres-Hebdo/I+C over the 2001-2010 period. Additional data have been graciously provided by IPSOS Média CT (Pôle Culture). We would like to express our thanks to Emmanuelle Godard for bearing with our requests.

1. IPSOS or GfK ?

Every year, just before the opening of the Angoulême Festival, the two competing poll institutes reveal their key figures for the bande dessinée market. And every year, as the presented data sometimes appear significantly different, it is the same question : who is to be believed ? And, in the more specific case of this “Numerology”, does choosing the more complete IPSOS data over GfK’s introduce any bias in our assessment of the market ?

Both institutes propose a “retail panel” service, which is defined as follow on GfK’s website[24] :

“This is a permanent and representative sample of retail outlets, in which observations on markets, product types, brands, references, price bands, are conducted on a regular basis.

-> Sample : the fraction of a statistical universe (the population of retail outlets)

-> Permanent : the individual in the panel are stable over time

-> Representative : data collected at retail outlets are extrapolated to be representative

-> Retail outlets : excluding wholesalers”

For reference, IPSOS MediaCT’s panel covers 2,400 retail outlets, representative of the traditional book retail chains (bookstores, specialized stores, big-box stores). Since January 2010, it also includes online sales. Regarding GfK’s panel, it claims over 3,500 retail outlets, with a cover rate of 98 % on the book market (excluding school books and mail order).

For both panelists, it starts up with a sample of retail outlets and their sales data — that is, an incomplete picture of the market, which is afterwards corrected through an in-house model. This model is regularly confronted with information gathered at publishers on their own sales, so that to check on its validity. Yet, each of these steps potentially introduces mistakes or rounding errors, meaning that the figures released by either GfK or IPSOS are estimates, and therefore include a margin for error.

In order to statute on the differences between the two visions of the bande dessinée market, we have chosen to compare periods for which we have corresponding figures — that is, the evolution of the global market over 2006-2010, and the best-selling titles list for the years 2006 and 2009.

For the market as a whole, we note that the given figures are significantly different, even when taking into account Internet sales (covered by GfK, but only included in IPSOS since 2010). The bande dessinée market in France is given around 39 million books for 400 million euros according to GfK, versus 33 million books and 340 million euros for IPSOS (corrected with Internet sales). Nevertheless, this gap is stable over the past few years, IPSOS’ estimate representing around 87 % of GfK’s vision.

Yet, the evolution dynamics are again significantly distinct : GfK sees a bande dessinée market in units on near-constant decline since 2004 (with the exception of a minimal regain in 2009) ; to the contrary, IPSOS observes a progression in unit sales until 2007, followed by three years of decline. Over 2006-2010 though, both institutes register a similar evolution (significant decrease of unit sales in the face of growing value sales), but markedly more important for IPSOS : -2.7 %(u)/ +5.1 %(€) versus -8.1 %(u)/+4.4 %(€) for GfK. Correcting IPSOS data to cover Internet sales does not alter the picture, resulting on a market down in units (-3.3 %) and notably up in value (+10.3 %).

Two other observations : frist, IPSOS and GfK present similar estimated for average retail prices, both for the overall market and for the two segments of manga and albums (i.e., non-manga). Yet, there is a slight difference regarding the market share of the manga segment, with GfK tending to be more optimistic by about 2 % against IPSOS.

Regarding the best-selling titles, there are also a few differences, but the overall view is very similar (please note that this study will be limited to unit sales, as value sales were not available to us). For 2006, GfK’s Top 20 sales for the year include the same titles (with a few ranking differences) as IPSOS’ ; for 2009, there is only a single title in IPSOS’ Top 20 which is not featured among GfK’s Top 20 sales for the year (Silex and the city, by Jul at Dargaud). Finally, in 2006 as well as in 2009, the top 5 titles are identical for the two institutes.[25]

The announced unit sales are also very close : for 2006, IPSOS’ estimated sales for the Top 20 titles was in average 90 % of those of GfK (with a 5 % standard deviation) ; for 2009, the ratio was 93 % in average (with a 6 % standard deviation). Yet, IPSOS seems to slightly minimize the sales of Naruto (the only manga title in those tops) when compared with GfK, with estimates at 89 % for 2006 and 89 % for 2009. For reference, the remainder of the Top 20 was estimated at 95 % for 2009.

Finally, considering overall series sales (and not just new releases), it appears a situation similar to that of the overall market : IPSOS estimates representing in 2009 87 % in average of GfK’s (87 % for 2008) with an 8 % standard deviation (versus 4 % for 2008). Overall, IPSOS data give slightly less importance to manga series (84 % in 2009, 86 % in 2008) than to the remainder of the market (86 % in 2009, 88 % in 2008) when compared with GfK.

The small gap between the sales figures of the two institutes for new releases can be surprising, especially when considering that accounting for Internet sales for 2009 would place IPSOS’ Top 20 at 98 % of GfK’s estimates, with series around 90 % and the overall market at 87 %. This apparent over-representation of new releases to the detriment of the back-catalog can in fact be explained by the variable impact of online sales : indeed, GfK indicated that online sales present the “long tail” phenomenon, and therefore favor back-catalog over new releases.

In fact, when neglecting the impact of online sales on new releases, sales by series are down to an 88 % ratio (with a 9 % standard deviation) for 2009 between IPSOS’ and GfK’s vision. On the new releases front, IPSOS’ view gives an increased importance (by about 5 %) for its Top 20 against GfK’s.

To conclude, we can safely say for the 2006-2010 period :

– Overall, GfK and IPSOS data are consistent and present strong similarities, indicating close views on a same market reality ;

– Even accounting for the different perimeters covered by both institutes (GfK including online sales), IPSOS’ vision for the market is more conservative than GfK’s, by 13 % in average. In detail, the manga segment is slightly under-represented by IPSOS (or over-represented by GfK) by about 2 % ; and new releases are over-represented by IPSOS (or under-represented by GfK) against back-catalog by about 5 % ;

– Finally, the best-seller charts are very close, as they feature the same titles ranked in a very similar order ; moreover, unit sales are very comparable between the two institutes, with IPSOS’ estimates representing an average 93 % of GfK’s for 2009.

In the light of those comparisons, it appears that both visions of the bande dessinée market in France, from IPSOS and GfK, while different, are consistent, a fact reflected in the comparable conclusions put forward by either institute in their respective communication. Notwithstanding some peculiarities linked to differences in the considered perimeters, they represent the same reality and are therefore both valid in their estimates.

We consider that our choice to focus on the available IPSOS data does not invalidate the pertinence of the analyses we could make, and that it is highly probable that the study of corresponding GfK data would lead to similar conclusions.

We would like to thank Emmanuelle Godard (at IPSOS) and Virginie Thibierge (at GfK) for their reactivity and patience in the face of our numerous enquiries.

2. Consumer panels

While the Livres-Hebdo/I+C panel focuses on tracking the evolutions of the market in terms of sales, a certain number of studies try and analyze the population of comic book buyers and/or readers.

Indeed, the number of comic book buyers in France remains stable, representing around 10 % of the total population. (cf. “Le marché du livre en 2006” [The book market in 2006], study from TNS-Sofres, which confirmed a similar ratio over 2007.)

Regarding the comic book readership, the study “Les pratiques culturelles des Français à l’ère numérique” [Cultural activities of the French in the digital age] conducted by the Ministry of Culture and the INSEE (published October 2009) indicates that only 29 % of the French population aged 15 or more have read a comic book over the past twelve months (cf. this chart).

3. What about the other countries ?

A recurring attack against the IPSOS figures is that they only cover the French market, and do not account for the Belgian, Swiss and Canadian market. And that would inevitably invalidate the analyzes done on that truncated base. Yet, it is important to note that France represent more than 80 % of this francophone space, both in terms of population and in terms of book market — as well as bande dessinée.

Indeed, the French metropolitan population represents 62 million inhabitants, while the cumulated French-speaking populations of Belgium, Canada and Switzerland only represent 13.4 million souls.[26]

Moreover, an estimate of the French language book and bande dessinée market indicated for 2006 (in millions of euros) :[27]

||French language market (in millions of euros)||

|2006|France|Belgium|Switzerland|Canada|Total|France Share|

|Total books|4,100.0|253.4|77.9|328.0|4,768.9|86 %|

|Bande dessinée|300.0|38.7|11.9|16.4|367.0|82 %|

Of course, each territory presents its own specificities, and the trends observed with the Livres-Hebdo figures only cover the French market. Yet, this market has an overwhelming importance in the whole picture. For instance, to compensate a 5 % variation observed on the French market, the other three countries would have to present a variation of 23 % in the opposite direction.

Considering its weight (over 80 % of the French-language bande dessinée market), the evolutions of the French market therefore have an immediate (and important) impact on the industry in general.

4. The share of online sales

Internet penetration in households in France has seen a strong evolution over the past years, rising from 16 % in 2002 to 48 % in 2007. Following this progression, the general market has seen part of its revenue moving online over the past years, a part that was not covered by the Livres-Hebdo/I+C panel until 2010. For 2010, IPSOS estimates the share of online sales amounting to around 7.5 % of the overall activity.

As indicated above (see “IPSOS or GfK ?”), online sales follow very specific dynamics (known as the “long tail effect”), and see increasingly scattered sales in favor of references with very low levels of activity. If about 7.5 % of the total bande dessinée market is now sold through online sales, it is therefore probable that the importance of online sales for the best-selling titles is lower than this ratio.

It is important to keep in mind this market mutation, in particular when comparing different periods — a sales gap (downward) around 5 % between the years 2001-2002 and the years 2008-2009 is likely not significant.

Notes

- “La fin de la bulle”, Fabrice Piault and Anne-Laure Walter, Livres-Hebdo #849 (January 21, 2011), pp.71-76.

- The column “’10”corresponds to the title released in 2010. Previous titles in the series are listed under “N-1” for the penultimate, “N-2” for the previous one, and so on until “N-5”.

- During a conference on “Bande dessinée : between heritage and digital age”, which was held at the Bibliothèque nationale de France on October 5th, 2010. We want to take the opportunity to warmly thank Martin Zeller for the constructive exchanges on the subject.

- As it has been the case with Tintin (single volume or small albums) or Gaston (new, revised and renumbered edition) over the past years.

- And also allow reducing the number of references within a given series. This simplifies the task at hand for the whole chain, which has to face an ever-increasing number of references to deal with.

- I.e. for the period from August 20th to December 31st of the corresponding year.

- This entry covers the series Joe Bar Team, Blacksad and Les Bidochon, which benefit from important print runs but present erratic publishing schedules. For example, the 7th volume of Joe Bar Team released in 2010 was the first in six years.

- In fact, Dargaud did indeed manage to “stick to the plan” in terms of new releases, going from 105 titles in 2009 to a mere 111 for 2010. Nevertheless, the number of republishing titles has more than doubled over the same period, going from 47 in 2009 to 108 for 2010. Resulting in a net growth of 44 % for the overall number of releases.

- Le Comptoir des Indépendants, Makassar, La Diff, or even Harmonia Mundi. This list not aiming at being exhaustive, of course.

- DDL Diffusion, Delsol, Glénat Diffusion, Flammarion Diffusion, to only cover those belonging to the five largest bande dessinée publishing groups.

- This phenomenon is visible when considering the structure of the yearly Top 50 published by Livres-Hebdo. Over the 2001-2004 period, about 20 of the Top 50 sales for the year came from the back-catalog. Since 2007, this number is down to 11 titles released prior to the current year among the Top 50 best-sellers, indicating an increased bonus for new releases.

- I.e. Atrabile, Cornélius, Drozophile, Ego comme X, FRMK, Groinge, L’Association, Le Cycliste, Les Requins Marteaux, Mosquito, Rackham, Six Pieds Sous Terre, and Vertige Graphic.

- Including Les 400 coups, Actes Sud, Beaulet, La Boîte à bulles, Ca et là, Café Creed, Cambourakis, Des Ronds dans l’O, Diantre, FLBLB, IMHO, La Cinquième Couche, La Pastèque, L’An 2, L’Employé du moi, Les Enfants rouges, Les Impressions nouvelles, Les Rêveurs, Le Lézard noir, Mécanique générale, Sarbacane, Thierry Magnier, Warum.

- I.e. Drugstore (Glénat), Ecritures (Casterman), Expresso (Dupuis), Futuropolis (Gallimard-Soleil), Bayou (Gallimard Jeunesse), KSTR (Casterman), Outsider (Glénat), Poisson Pilote (Dargaud), Quadrants (Soleil), Rivages noir (Casterman), Sakka (Casterman), et Shampooing (Delcourt).

- Available online at (in French

- Monitoring conducted yearly by Mangaverse.

- Available online.

- That is, Hanawa Kazuichi, Kamimura Kazuo, Tezuka Osamu, Ishinomori Shôtarô and Shirato Sampei — with the addition of Koike Kazuo, writer on Lady Snowblood.

- Since September 2009, three trilogies by Kamimura Kazuo (Lorsque nous vivions ensemble, Folles Passions and La Plaine du Kantô), two tetralogies (Ishinomori Shôtarô’s Sabu & Ichi and Shirato Sampei’s Kamui-den) and two one-shots (Ishinomori’s Hokusai and Kamimura’s L’Apprentie Geisha) have been added to the collection.

- In spite of the small advantage of the first-time inclusion of online sales in the announced figures. Yet, considering that “long tail” dynamics are at work on this retail channel, it is highly probable that its impact is significantly lower than the 7.5 % contribution estimated for IPSOS for the overall market.

- The only exception is of course the peculiar case of Marjane Satrapi’s Persépolis, which probably relied on consumption dynamics significantly different from that of mainstream products.

- At the heart of the Livres-Hebdo yearly feature for 2009 (titled “Un virage très net”, which roughly translates to : “The online move”), the digital question is barely touched in the 2010 edition (“at a time where digital investments remain important”) before moving on to media-mix and other types of adaptations. Such a deafening silence usually indicates a less-than-stellar commercial performance…

- Available online (in French) at the address .

- Though sales data for 2010 were not available by the time of this study, the situation is the same for 2010 : a common Top 10 for GfK and IPSOS, and a single difference among the Top 20 sales for the year (Les Légendaires #12 at Delcourt in IPSOS’ top, replaced by Le Livre d’Or d’Astérix in GfK’s).

- Belgium : 10.4m inhabitants, with 40 % of French-speakers ; Canada : 33.2m inhabitants with 23.2 % of French-speakers ; Switzerland : 7.6m inhabitants with 20.4 % of French-speakers.

- Sources : France, SNE ; Belgium, Le marché du livre de langue française en Belgique (données 2006) ; Switzerland, Etude de l’Université de Zurich sur le marché du livre en Suisse ; Canada, Le marché du livre au Québec.